About the Author: John Miller

Last updated: September 5, 2025

Reading Time: 8.5 minutes

What Is Invoice Factoring?

At some point, nearly every business needs a capital boost whether it is to meet payroll, launch a new project, or simply cover day to day operations while waiting on customers to pay. For many small and midsize businesses, traditional bank loans are not always within reach. High credit score requirements, long approval times, and the need for substantial collateral can create roadblocks.

That is where invoice factoring enters the picture.

Invoice factoring is a financing method where a business sells its outstanding customer invoices to a third party known as a factoring company for a cash advance. Typically, this advance amounts to 80% to 90% of the invoice’s value. Once the factoring company collects payment from your customer, you receive the remaining balance, minus a small factoring fee.

Unlike a loan, factoring does not create debt. It is simply a way to unlock cash that is already earned but tied up in accounts receivable.

Invoice Factoring vs Bank Loans

While both factoring and bank loans can provide working capital, the two differ greatly in how they are structured and who they serve best. Here is how they compare:

| Invoice Factoring | Bank Loans | |

|---|---|---|

| Approval Speed | Often approved in 24 to 48 hours | Can take weeks or months |

| Collateral | Only your receivables | Requires hard assets |

| Debt Incurred | No debt involved | Adds to your liabilities |

| Credit Requirements | Based on your customers’ credit | Based on your credit history |

| Flexibility | Grows with your receivables | Fixed loan amount |

| Cost | 0.5% to 3.0% of invoice value | Varies by interest rate and credit |

| Accessibility | Great for newer or credit challenged businesses | Best for established businesses with strong credit |

Approval Process

Factoring: One of the biggest advantages of factoring is how quickly you can get approved. There is not a very long application process. At Porter Capital, we can often approve and fund a business in as little as 24 hours.

Bank Loans: Banks, on the other hand, require extensive paperwork and financial documentation. The process can take weeks and even then, approval is not guaranteed, especially for businesses without years of strong financial performance.

Credit Requirements

Factoring: Your business credit is not the focus your customers’ payment history is. This makes invoice factoring a viable option for businesses that might still be building credit or recovering from setbacks.

Bank Loans: Banks assess your personal and business credit scores, financial statements, and often your business plan. If your credit profile is not spotless, getting approved can be tough.

Structure

Factoring: As your business grows and generates more invoices, your available funding grows with it. This means your access to working capital scales in real time with your sales volume.

Bank Loans: Bank loans are static you get a fixed amount, and once you hit the limit, you will need to apply again if you need more. That rigidity can create cash flow bottlenecks.

Cost

Factoring: Costs can vary, but typically range from 0.5% to 3.0% of the invoice’s face value. If your customers pay quickly, your costs are lower. And since factoring is not debt, there are no interest payments just a fee for the advance.

Bank Loans: Bank loans often come with lower interest rates, especially if you have excellent credit. However, the overall affordability depends on the terms, fees, and your ability to qualify for competitive rates.

Should You Choose Factoring or a Bank Loan

Businesses That Are a Fit for Factoring

Factoring tends to be a great solution for:

-

Startups and small businesses

-

Companies experiencing rapid growth

-

Businesses with long payment cycles

-

Organizations that need fast flexible funding

If you are dealing with slow paying customers or need cash now to take advantage of a growth opportunity, factoring offers immediate liquidity without waiting on bank approval or taking on new debt.

Businesses That Are a Fit for Bank Loans

Bank loans are typically a better fit for:

-

Well established companies

-

Businesses with strong credit and ample collateral

-

Companies needing long term capital at lower cost

If you qualify for a favorable loan and do not need funding quickly, this can be a cost effective solution.

If the Bank Says “No”

If you have already applied for a loan and been turned down, you are not alone. Many businesses find themselves shut out due to credit issues or lack of collateral. But that does not mean your financing options are exhausted.

At Porter Capital, we have helped countless businesses who were declined by their bank. Factoring allows us to step in and provide funding where traditional lenders cannot. We work with business owners every day to create cash flow solutions that do not require perfect credit or long histories.

Invoice factoring is essentially a sale of receivables not a loan. It means selling unpaid invoices to a factoring company for immediate funds, providing businesses with instant cash flow by converting their receivables into cash quickly. This helps businesses manage cash flow issues and cover short term expenses, making it an essential tool for operations and growth.

Definition of Invoice Factoring

Invoice factoring is selling unpaid invoices to an invoice factoring company at a discount. Factoring companies buy these invoices and provide immediate cash flow to businesses.

Unlike traditional loans, invoice factoring is legally classified as a sale of invoices, not a debt instrument, which is different from conventional borrowing methods.

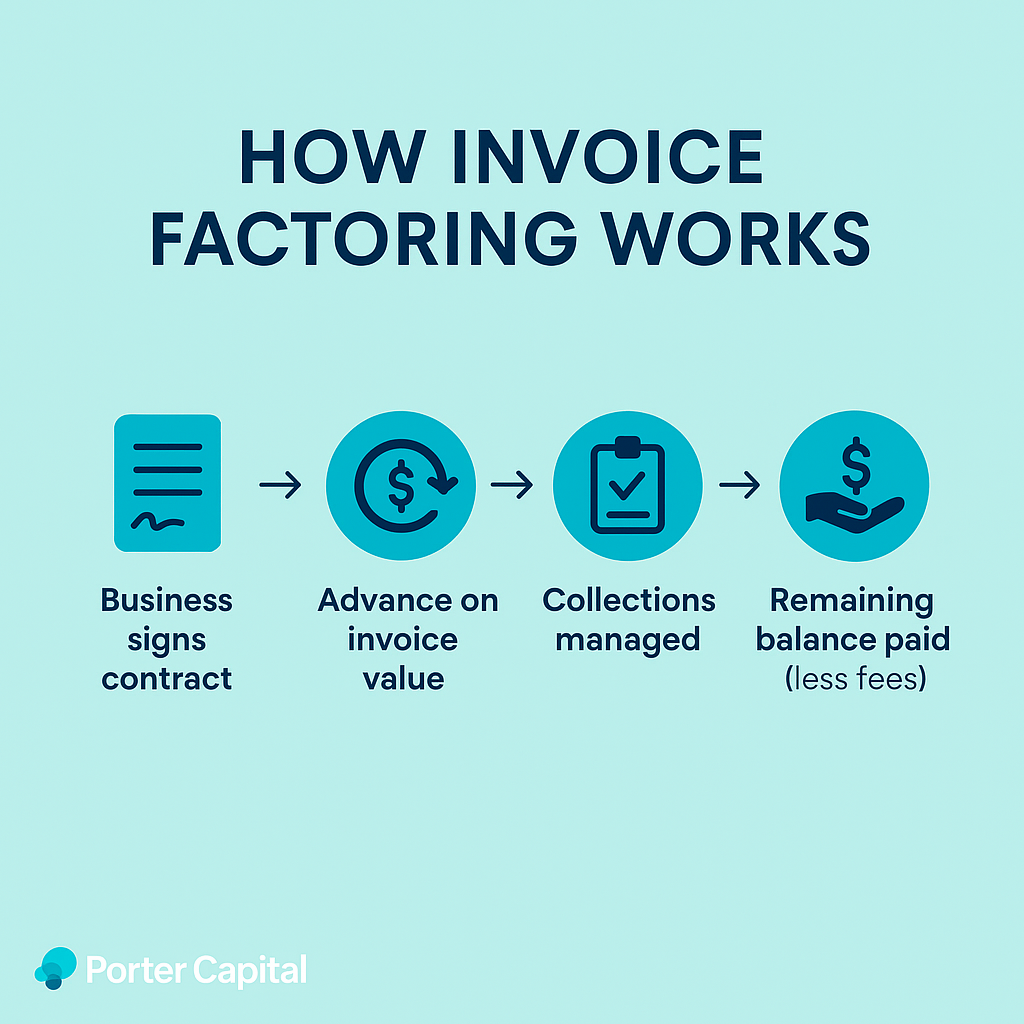

How Invoice Factoring Works

Invoice factoring starts with the business signing a contract with a factoring company. The business then gets an advance on the invoice amount, usually 70% to 90% of its value. The factoring company takes over collections from customers, managing payments efficiently.

Once the customer pays, the factoring company pays the remaining balance to the business, minus their fees. This simplifies the business’s work and boosts working capital.

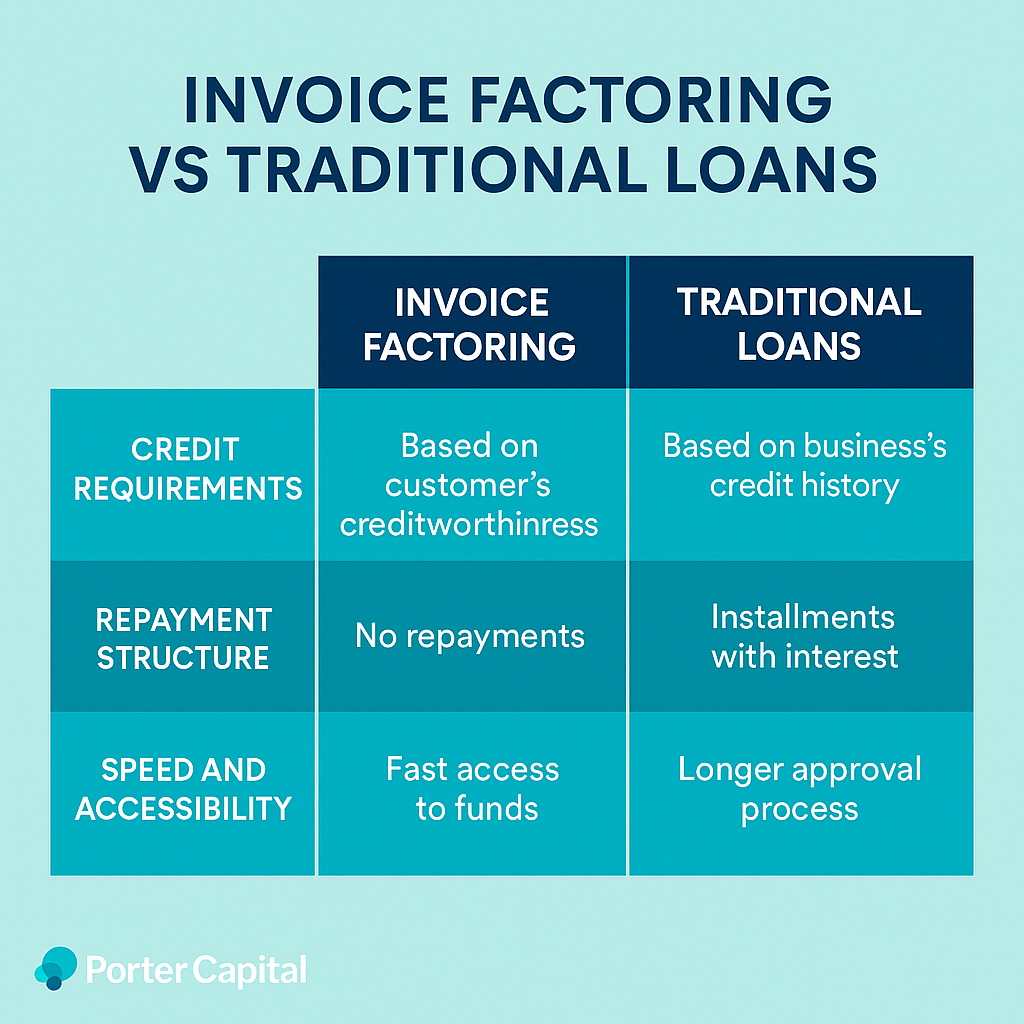

Invoice Factoring vs Traditional Loans

Invoice factoring and traditional loans have many differences. Invoice factoring means selling unpaid invoices for immediate cash, while traditional loans are borrowed funds repaid over time with interest.

Knowing these differences will help businesses make better financial decisions.

Is Invoice Factoring Debt?

Invoice factoring is not debt. It’s the sale of accounts receivable not borrowing money.

This is important for businesses that want to control their finances without increasing liabilities.

Legal Classification

Legally, invoice factoring is a sale of receivables. There is no repayment involved as businesses sell their unpaid invoices to a factoring company for immediate cash. This is different from traditional debt instruments making it a unique receivable financing option.

Impact on Business Finances

Invoice factoring affects business finances by transferring receivables ownership to the factoring company. This provides immediate working capital through selling accounts receivable financing and accounts receivable factoring without increasing balance sheet debt.

In recourse factoring, businesses must repay the factor for any unpaid invoices which can affect financial planning.

Types of Invoice Factoring

Understanding the different types of invoice factoring is crucial to choose the right one for your business. Common types are recourse factoring, non-recourse factoring and spot factoring.

Recourse Factoring

In recourse factoring, the business is liable for unpaid invoices. This option usually has lower fees than non-recourse factoring but the business must cover any losses from uncollected invoices.

Non-Recourse Factoring

In non-recourse factoring, the factoring company assumes the risk of non-payment by customers. This option is more expensive as the factoring company takes on more risk but provides businesses protection against client non-payment.

Costs of Invoice Factoring

Invoice factoring has various costs businesses need to consider, including invoice factoring cost. Typical factoring fees range from 1% to 5% of the invoice value per month depending on the invoice amount and the client’s creditworthiness.

Factoring Fees

Common fees in invoice factoring are service fees, processing fees and factoring fee charge fees. These fees can impact the overall cost of factoring so businesses should understand the fee structure and ask about any additional charges.

Advantages of Invoice Factoring

Invoice factoring has advantages like improved cash flow and easier qualification for businesses with poor credit.

Benefits

One of the primary benefits of invoice factoring is the immediate cash flow without increasing balance sheet liabilities. This is more beneficial for startups or businesses with poor credit, providing access to working capital without a strong credit history.

Choosing the Right Factoring Company

Choosing the right factoring company maximizes the benefits of invoice factoring. Evaluating the reputation, fee structures and industry experience of different factoring companies helps align their services to your business needs.

Evaluating Factoring Companies

Consider the reputation, advance rates and customer support quality when evaluating factoring companies.

Check if they specialize in your industry as this can affect service quality and cost.

Questions to Ask

Questions to ask potential factoring partners are their policies on recourse and non-recourse factoring, the flexibility of their funding solutions and transparency in their terms and conditions to avoid hidden charges.

In Summary Factoring vs Bank Loans

Factoring and loans serve different needs, and understanding those differences helps you make the best decision for your business.

Factoring is best when:

-

You need quick cash flow

-

Your business is growing

-

You have reliable customers but limited credit history

Bank loans work well when:

-

You are established and have strong credit

-

You need long term financing

-

You have time to wait for approval

There is no one size fits all solution but if you are looking for fast flexible funding that does not saddle your business with debt, factoring may be the better fit.

FAQs

What is a factoring loan

Technically, a factoring loan is a misnomer. Invoice factoring is not a loan. It is the sale of your receivables to get an advance on unpaid invoices. There is no repayment obligation your customers pay the factor directly.

Is factoring considered debt

No. Because you are selling invoices, not borrowing against them, factoring does not add liabilities to your balance sheet.

Why might a company choose factoring instead of a loan

Factoring provides quicker access to capital, is easier to qualify for, and adjusts to your cash flow needs. For companies in a growth phase or struggling to get traditional financing, it can be the difference between stagnation and success.